ZKsync and BitGo Bring Bank Deposits Onchain

ZKsync and BitGo build a compliant system for tokenised deposits, combining custody, privacy, and blockchain settlement within existing banking frameworks.

×

×

Join Our Internship Program

Apply Now →Banks have spent years circling blockchain. The interest was always cheaper settlement, programmable treasury operations & 24/7 liquidity but the infra that could deliver those things inside a banking environment did not exist in a form institutions could deploy without taking on enormous compliance risk.

The partnership announced on March 25, 2026 between BitGo & ZKsync is a direct attempt to change that combining institutional custody with a privacy-preserving permissioned blockchain to give banks a complete stack for tokenised deposits, built to sit entirely within existing regulatory frameworks.

- What the Two Sides Each Bring

- How Tokenised Deposits Actually Work in This Model

- What Makes This Different From Stablecoins

- Where This Sits in the Broader ZKsync Strategy

What the Two Sides Each Bring

The partnership works because the two companies solve different parts of the same problem.

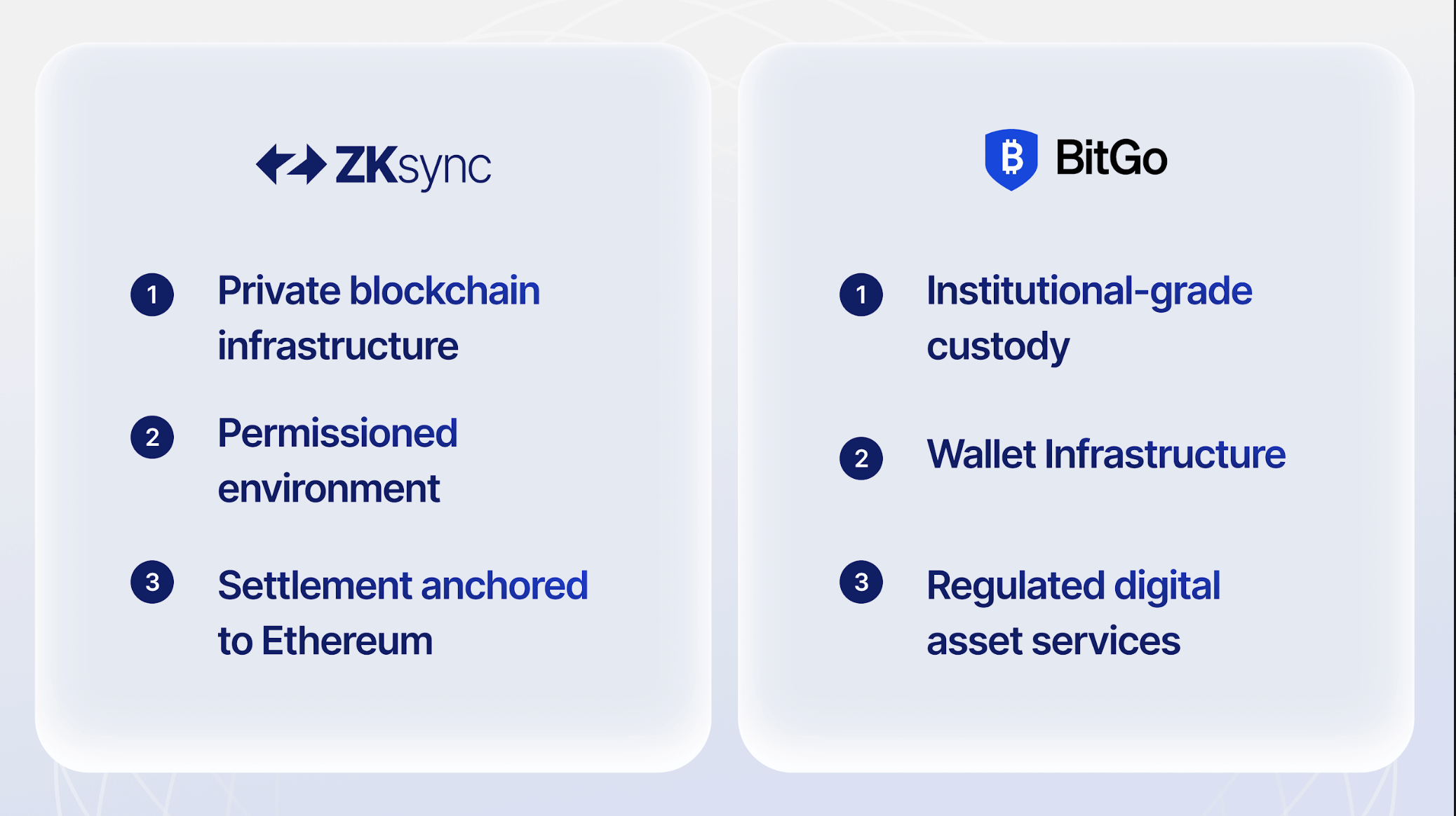

BitGo is one of the oldest institutional custody providers in the digital asset space, twelve years of operation, zero security incidents, roughly $104 billion in assets under custody & approximately 4,900 institutional clients including some of the largest banks & asset managers in the world. When a bank needs to hold digital assets or issue digital liabilities, BitGo is the layer that handles the wallets, the key management & the regulated custody infrastructure. It is the part that banks already understand & trust.

ZKsync's contribution is Prividium, the permissioned, privacy-preserving blockchain built by Matter Labs specifically for regulated financial institutions. Prividium runs inside a bank's own controlled environment. Transactions are processed privatelyand only zero-knowledge proofs leave that environment to be anchored on Ethereum. No transaction data is ever exposed on a public network. Regulators can be granted selective disclosure access. The bank retains full control over who participates.

Together the two layers give a bank something it could not build alone in any reasonable timeframe: a production-ready, compliance-first system for issuing, transferring & settling tokenised deposits with enterprise-grade throughput, near-instant finality, & full KYC/AML built into the protocol itself.

A big step forward for the digital assets industry and U.S. banking.

ZKsync × @BitGo partner to deliver a production-ready solution for tokenized deposits, combining secure custody with private, compliant blockchain settlement.

Built for banks. Ready for deployment. pic.twitter.com/SBQQXHmEya— ZKsync (@zksync) March 25, 2026

The technical specifications that ZKsync published alongside the announcement are worth noting. Settlement happens in approximately one second. Fees sit below $0.001 per transfer. The system supports atomic settlement, meaning both sides of a transaction either complete simultaneously or neither does across chains. And the team cites a 30 to 50 percent improvement in liquidity utilisation through instant collateral repledging, which matters significantly for treasury operations where efficiency is a constant pressure.

How Tokenised Deposits Actually Work in This Model

A digital token that represents a bank deposit, backed one-to-one by fiat held in the regulated banking system. It stays on the bank's balance sheet. It carries the same customer protections & FDIC-style safeguards as the underlying deposit. It does not exist outside the banking system in any meaningful sense.

What it gains by being tokenised is programmability & speed. Smart contracts can execute treasury rules automatically. Transfers that currently take a business day can settle in seconds. Payments can be structured with conditions attached, executing only when both sides of a transaction are confirmed. The bank does not give up control or compliance to get these capabilities but it does get them while keeping everything it already has.

The operational flow: Banks issue tokenised deposits on Prividium. A clearing layer manages fungibility and net settlement across participants. corporate wallets hold those deposits alongside other assets, smart contracts handle the treasury logic. Settlement happens in seconds rather than days. The entire process runs inside the bank's permissioned environment, with Ethereum providing the security anchor through ZK proofs.

Chen Fang, BitGo's Chief Revenue Officer, put it plainly: financial institutions need infrastructure that brings blockchain efficiency into existing banking models without compromising control, security, or regulatory alignment.

What Makes This Different From Stablecoins

The distinction between tokenised deposits & stablecoins is one that the banking industry cares about deeply, & it is worth being precise about.

A stablecoin is a liability of the issuer, Circle, Tether, whoever created it, tt exists outside the traditional banking system. If the issuer fails, the exposure sits entirely outside the protections that govern bank deposits. For regulated banks, this is not an acceptable structure. Taking on stablecoin exposure means taking on credit risk to a non-bank entity operating under a lighter regulatory regime.

A tokenised deposit stays inside the bank. It is the bank's own liability, governed by the same rules, the same oversight, & the same protections as any other deposit the bank holds. The bank does not outsource its balance sheet to a third party. It retains the relationship with its customer & the regulatory status of those funds.

This is not a subtle distinction. It is the entire reason institutions that cannot use stablecoins can use tokenised deposits. The blockchain benefits are added on top of an existing structure that regulators already understand, rather than replacing it with something they do not. The SEC has made clear that securities laws apply to tokenised instruments regardless of the technology underneath them, which reinforces why the regulatory preservation in this model matters so much to institutional buyers.

Alex Gluchowski, Matter Labs CEO, described it as how banks bring money onchain without leaving the regulatory system. That sentence is doing a lot of work, & it is accurate.

Where This Sits in the ZKsync Strategy

This is not ZKsync's first move in the institutional tokenised deposit space. In March 2026, the Cari Network announced it was building its tokenised deposit infrastructure on Prividium. We covered the full picture of how ZKsync is bringing private blockchain settlement to U.S. banks when that story broke.

The BitGo partnership is the custody layer that turns Prividium from a compelling protocol into a fully deployable bank product. Without institutional custody that banks already trust, Prividium is a blockchain looking for adoption with BitGo providing the regulated wallet & custody infrastructure alongside it, the combined offering becomes something a bank's compliance team can approve & its treasury team can actually use.

BlackRock CEO Larry Fink has called tokenisation essential to the next phase of global finance, citing emerging markets as leading the way. The infrastructure ZKsync & BitGo are building is precisely the kind of compliant, bank-native on-ramp that makes that vision practically achievable for regulated institutions.

The solution is currently in testing with regulated financial institutions. Broader production rollout is targeted for later in 2026. No specific bank pilots have been named publicly yet. But the pattern of announcements over the past month Cari Network, the DC Blockchain Summit keynote & now BitGo suggests ZKsync is systematically assembling every component of the institutional stack before a larger wave of bank deployments is announced.

If you find any issues in this article or notice missing information, please feel free to reach out at team@etherworld.co for clarifications or updates.

To promote your Web3 articles, events, & projects, you may reach out anytime via EtherWorld PR for submissions & collaboration.

Related Articles

- ZKsync Brings Private Blockchain Settlement to U.S. Regional Banks

- India Spotlighted as BlackRock CEO Larry Fink Calls Tokenization Essential

- SEC Reaffirms Securities Laws Apply to Tokenisation

- US Banking Regulators Clarify Capital Treatment for Tokenized Securities

To follow blockchain news, track Ethereum protocol progress, and read our latest stories, subscribe to our weekly today.

Disclaimer: The information contained in this website is for general informational purposes only. The content provided on this website, including articles, blog posts, opinions, & analysis related to blockchain technology & cryptocurrencies, is not intended as financial or investment advice. The website & its content should not be relied upon for making financial decisions. Read full disclaimer & privacy policy.

To stay updated on blockchain news, Ethereum protocol progress, and our latest stories, subscribe to our weekly digest and YouTube channel for ELI5 content.

To promote your Web3 articles, events, project updates, and Press Releases, reach out anytime via EtherWorld PR for submissions and collaboration. For other queries, email contact@etherworld.co.

If you’d like to support our work, share the content and consider donating at avarch.eth.

Join our community on Discord and follow us on Twitter, Facebook, LinkedIn & Instagram.