Ethereum Staking in 2026

Ethereum staking in 2026 evolves beyond passive yield into a complex ecosystem balancing liquidity, validator sovereignty, reusable security, & layered DeFi-driven capital efficiency.

×

×

Join Our Internship Program

Apply Now →In 2026, Ethereum staking will be more than just a Proof-of-Stake passive yield mechanism. Liquidity, validator infrastructure, economic security, and DeFi capital efficiency are now closely related to one another in this intricately intertwined financial and security architecture. What started off as a simple Ethereum block validation system has evolved into a whole ecosystem centred on liquid collateral, reusable trust, and layered staking rewards.

The most significant change is that staked ETH is now dynamic. Staking used to include locking ETH into validators and obtaining native rewards that were comparatively predictable. These days, that same ETH may secure Ethereum, produce liquid staking derivatives, take part in DeFi loan markets, and use restaking infrastructure, such as EigenLayer, to protect external systems. In essence, Ethereum staking has evolved into a programmable financial system.

The difference between solo staking, liquid staking, and restaking will be crucial in 2026 because of this change. These models are not interchangeable and compete only on APR. Regarding custody, decentralisation, liquidity availability, validator ownership, and systemic risk exposure, each one represents a radically different strategy.

Self-sovereignty and direct validator engagement are given priority in solo staking. Liquid staking uses tokens like stETH and rETH to promote composability and liquidity. By enabling previously staked ETH to secure further decentralised systems using reusable economic security models, restaking aims to maximise capital efficiency.

This progress was further expedited by the emergence of protocols such as Lido, Rocket Pool, ether.fi, and EigenLayer. Staked ETH was converted into extremely liquid DeFi collateral by Lido.

A more decentralised validator environment based on permissionless node participation was created by Rocket Pool. ether.fi blended restaking exposure with liquid staking. Through AVSs, or Actively Validated Services, EigenLayer created a whole new market for external validator security.

This implies that staking yields in 2026 can no longer be interpreted in a vacuum. A 12% restaking return and a 4% staking return are based on entirely different hypotheses on validator concentration, cutting exposure, smart contract dependency, and liquidity risk.

The ecosystem becomes increasingly focused on a single tradeoff as Ethereum staking develops: striking a balance between capital efficiency, liquidity, and sovereignty without creating unsustainable systemic fragility.

- Solo Staking: Sovereign Validation & Native Ethereum Security

- Liquid Staking: Unlocking Liquidity Through Staking Derivatives

- Restaking Compared: Reusable Economic Security & Layered Yield Dynamics

- Ethereum Staking Protocols in 2026: Risk, Yield, & Custody Dynamics

Solo Staking: Sovereign Validation & Native Ethereum Security

As solo staking requires direct validator operation and does not rely on other staking protocols, it continues to be the closest embodiment of Ethereum's original Proof-of-Stake goal. This approach allows the validator operator to actively participate in Ethereum consensus while retaining total control over validator infrastructure, staking keys, execution clients, and withdrawal credentials.

Solo staking, in contrast to pooled staking systems, views ETH more as validator infrastructure capital than as reusable financial collateral. As the majority of Ethereum's staking ecosystem now centres on layered liquidity and financialization, that distinction will become more crucial in 2026.

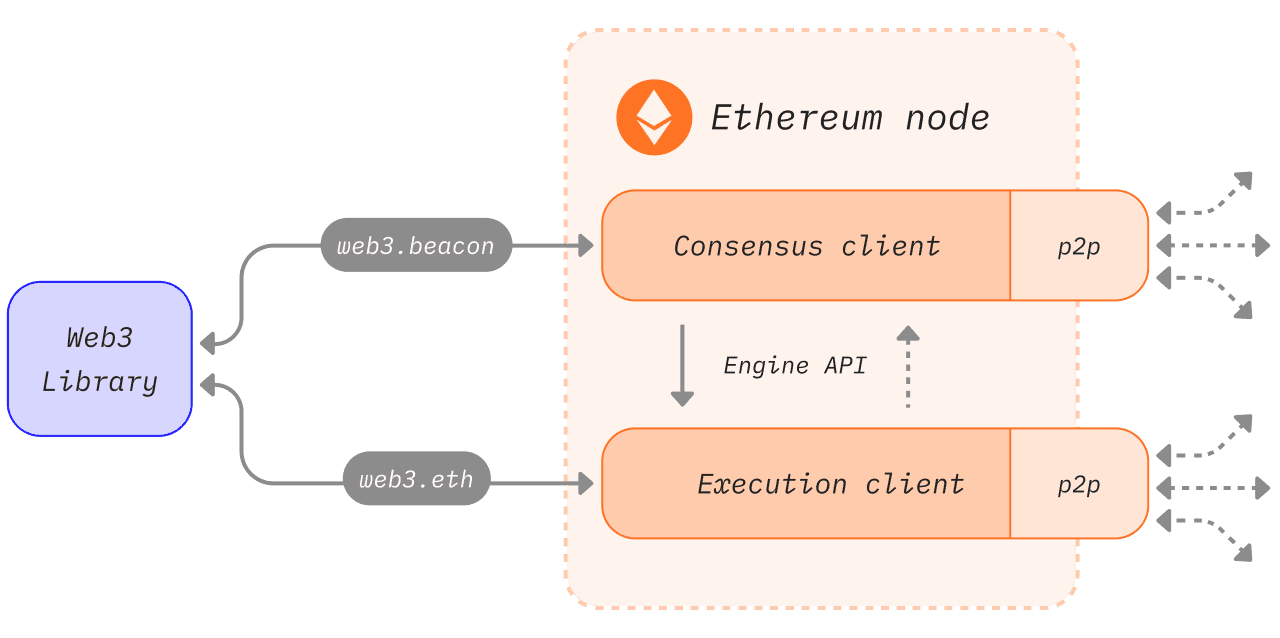

Source: Ethereum

Ethereum’s validator architecture requires synchronized operation between execution and consensus clients, highlighting the infrastructure complexity, monitoring requirements, and direct consensus responsibilities associated with solo staking.

Compared to other retail staking systems, solo staking has a far more difficult operational framework. Consistent uptime, secure infrastructure dependability, synchronisation of execution and consensus clients, continual monitoring of slashing conditions, and performance management are all requirements for validators. Ethereum was never intended for solo staking to be a source of passive income. Direct involvement in network security was the foundation of its design.

Many Ethereum-native players still believe that solo staking is the safest and cleanest long-term staking model because of this operational responsibility. Liquid staking derivatives, protocol governance dependencies, smart contract intermediate layers, and an external validator coordination architecture between Ethereum and the validator are all absent.

Risk isolation is the main benefit of solo staking.

Source: Lido

Only operational risks, including downtime fines, slashing incidents, hardware malfunctions, internet outages, or validator misconfiguration, are often present for a lone validator. The systemic financial contagion hazards that are now prevalent in liquid staking and restaking ecosystems are substantially avoided by solo staking.

Due to the tight integration of Ethereum staking with DeFi collateral markets, this will be more significant in 2026. The usage of liquid staking derivatives in collateralised borrowing systems, leveraged ETH loops, lending protocols, and rehypothecation structures is growing. The majority of solo staking takes place outside of these linked dependence chains.

Native Ethereum staking yields typically range from 3% to 4%, contingent on network activity and validator participation rates. In contrast to restaking environments, these yields seem conservative. However, protocol-level security alignment and decreased systemic dependency exposure come at the expense of capital efficiency in solo staking.

The largest obstacle is still liquidity.

Compared to liquid staking systems, ETH becomes comparatively inaccessible after it is committed to validator involvement. Without extra wrappers that drastically alter the nature of the staking position itself, solo stakers are unable to simultaneously deploy the same ETH across DeFi methods, lending platforms, or collateral markets.

This leads to a significant philosophical split within Ethereum staking. Ethereum security comes first in solo staking, followed by financial utility. By optimising ETH mostly for liquidity and reusable economic efficiency, liquid staking and restaking reverse that order.

Almost all current Ethereum staking debates are characterised by this distinction.

Liquid Staking: Unlocking Liquidity Through Staking Derivatives

Since liquid staking addressed illiquid capital, the biggest inefficiency in traditional staking, Ethereum underwent a fundamental transformation. Before the development of liquid staking methods, rewards increased gradually while ETH locked inside validators remained unreachable. Users were thus compelled to decide between financial flexibility and validator rewards.

By offering liquid staking tokens that represent staked ETH positions while being transportable and usable across DeFi ecosystems, protocols such as Lido and Rocket Pool eliminated the trade-off.

These protocols enabled staked assets to continue operating as profitable financial capital rather than requiring users to lock ETH within validators with no access to liquidity. Lido issues stETH, while Rocket Pool issues rETH, and both assets are designed to track the value of underlying staked ETH while continuing to generate validator rewards in the background.

By 2026, the majority of Ethereum staking activity will be controlled by liquid staking. DeFi composability was the main factor driving the expansion of liquid staking. Staking awards could now be earned by users while concurrently:

- providing liquidity,

- borrowing against staking positions,

- participating in leveraged ETH strategies,

- using staking derivatives as collateral,

- and deploying assets into yield-generating systems.

As a result, staking became a fundamental component of Ethereum's financial system. Lido's level of liquidity and ecosystem integration helped it become the most popular liquid staking protocol. StETH is firmly ingrained in:

- Aave,

- MakerDAO,

- Curve,

- collateral lending markets,

- institutional DeFi systems,

- and leveraged the ETH infrastructure.

Lido’s dominance was reinforced by consistent growth in stETH adoption across DeFi, with the protocol maintaining the largest share of liquid-staked ETH and deep integration into major Ethereum applications such as Aave, Curve, and MakerDAO, strengthening stETH’s role as a core source of collateral and on-chain liquidity throughout the ecosystem.

Source: Lido

Strong network effects resulted from these interconnections. In comparison to less liquid staking ecosystems, large positions may typically join and exit stETH marketplaces with less slippage. Because of this, significant ETH holders and institutions looking for scalable liquidity found Lido particularly appealing.

However, Lido's size also raised serious issues with protocol centralisation and validator concentration. One liquid staking mechanism handling a sizable portion of Ethereum staking raises long-term governance and systemic reliance issues for Ethereum.

Rocket Pool had a unique approach to liquid staking.

Rocket Pool placed more focus on decentralised validator participation through permissionless node operation than it did on institutional scale and liquidity domination.

Rocket Pool supports more than 620,000 ETH staked across over 19,000 validators distributed throughout 100+ global regions, highlighting the protocol’s emphasis on decentralized validator participation and infrastructure diversity. Rather than concentrating validation within carefully selected validator sets, this architecture distributes validator infrastructure more widely across independent operators.

Source: Rocket Pool

This distinction is both technical and philosophical. Market integration and liquidity efficiency are Lido's top priorities. Rocket Pool places a high priority on wider infrastructure dispersion and validator decentralisation.

Both approaches nevertheless have dangers that are not present in solo staking. Users of liquid staking are subject to temporary depeg events, governance dependence, staking derivative market volatility, and smart contract weaknesses.

Conceptually, the depeg issue is particularly significant. Despite representing underlying staked ETH, stETH and rETH are nevertheless exchanged on the market. These derivatives may briefly trade below ETH parity during times of market panic or liquidity stress. Even little variations can set off liquidation cascades over larger collateral systems in leveraged DeFi situations.

Ethereum staking was effectively converted into collateral infrastructure for decentralised finance through liquid staking. Significant capital efficiency was made possible by that invention, but it also brought financial contagion dynamics straight into Ethereum's staking layer.

Restaking Compared: Reusable Economic Security & Layered Yield Dynamics

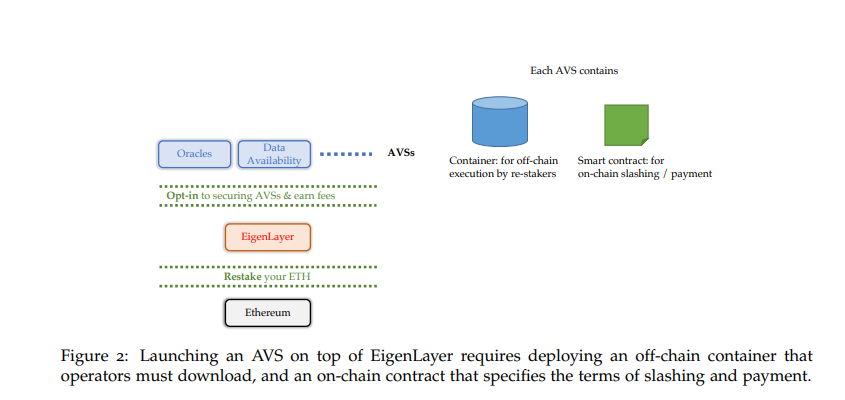

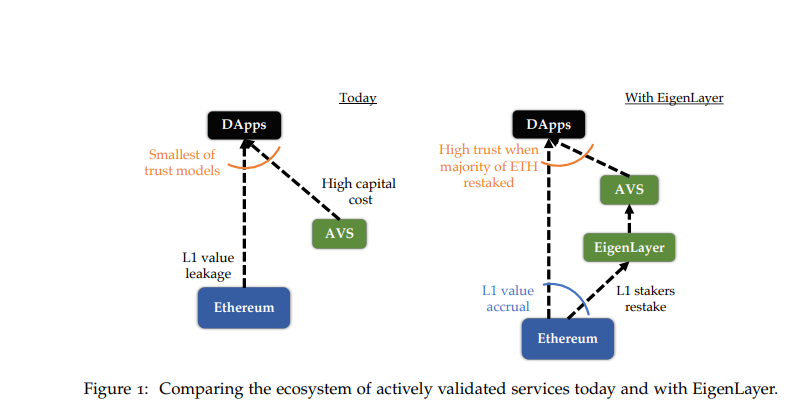

Because restaking significantly altered what staked ETH could secure, it became one of Ethereum's most significant structural improvements. Prior to EigenLayer's introduction of reusable economic security, Ethereum staking was mainly restricted to the Ethereum consensus. Ethereum blocks were secured by validators, who also received native protocol rewards.

That model was significantly expanded by Restaking. Through AVSs, or Actively Validated Services, EigenLayer developed a framework that allowed ETH that had previously been staked to secure additional decentralised infrastructure outside of Ethereum. Included in these systems are:

- Oracle Networks,

- middleware infrastructure,

- bridges,

- modular blockchain systems,

- data availability layers,

- and decentralised validation services.

As a result, ETH was converted from one-time validator collateral to reusable financial security.

This change basically transformed Ethereum's validator ecosystem into the fundamental infrastructure for external decentralised systems, making it extremely significant. Through restaked ETH, new decentralised services might inherit Ethereum-aligned security rather than starting from scratch with completely different validator economies. More restaking yield comes from this.

Users and validators who take part in restaking systems can get:

- native Ethereum staking rewards,

- AVS incentives,

- additional ecosystem rewards,

- token emissions,

- and external validator compensation.

Because of this, restaking yields in 2026 frequently outperform regular Ethereum staking returns by a significant amount. However, because restaking creates completely new slashing and dependence structures, there is a larger yield.

Conventional Ethereum staking primarily exposes validators to Ethereum consensus penalties related to validator misbehaviour or uptime. These responsibilities are extended into external systems through restaking. Penalties for AVS malfunctions, middleware interruptions, bridge infrastructure, or problems with external validator coordination may now be imposed on validators.

Correlated slashing risk was brought into Ethereum staking ecosystems as a result.

Multiple systems can be simultaneously secured by the same ETH. Because the same collateral foundation is recursively leveraged across overlapping trust assumptions, the effects of an operational failure in one interconnected layer may extend to a larger staking infrastructure.

The conceptual danger that distinguishes restaking is the recursive structure. ETH gets significantly more linked while simultaneously becoming significantly more capital efficient.

The development of liquid restaking systems like ether.fi was also accelerated by the rise of restaking. Through assets like eETH and weETH, these protocols maintain liquid exposure while automating EigenLayer involvement.

This led to another significant change in Ethereum staking since users may now get layered restaking rewards without manually managing validator participation. Alternatively, staking, liquidity, and exposure to restaking could all be found within a single integrated system. However, more systemic dependency layers are introduced with each new incentive tier.

Restaking users are subjected to:

- AVS slashing,

- smart contract vulnerabilities,

- cross-protocol contagion,

- liquid restaking token depegs,

- governance dependency,

- bridge exploits,

- and validator correlation risks.

For this reason, restaking emerged as one of Ethereum's most contentious issues in 2025 and 2026. It creates one of the most structurally complex risk scenarios Ethereum has ever seen, but it also represents one of the highest capital efficiency models ever implemented into blockchain infrastructure.

Ethereum Staking Protocols in 2026: Risk, Yield, & Custody Dynamics

Ethereum staking methods will no longer be distinguished solely by staking rewards by 2026. The market has developed into a variety of staking models based on capital efficiency, reusable economic security, validator decentralisation, and liquidity availability. Within Ethereum's financial and security ecosystem, Lido, Rocket Pool, ether.fi, and EigenLayer all provide distinct perspectives on how staked ETH should operate.

It is more than just yield that distinguishes these methods. Validator involvement, liquidity, custody, cutting exposure, and dependency risk are all handled differently by each system. While some protocols promote institutional-scale liquidity, others concentrate on layered restaking rewards or decentralised validator infrastructure. Because of this, it has become more deceptive to compare staking processes just based on APR in 2026.

Rocket Pool: Decentralized Validator Participation

In contrast to institutional-scale liquidity domination, Rocket Pool prioritised decentralised validator infrastructure when it came to liquid staking. While continuing to produce validator incentives, the protocol produces rETH, a liquid staking coin that represents staked ETH.

Rocket Pool emphasises permissionless node participation and wider validator distribution among independent operators, in contrast to highly centralised validator schemes. Ethereum-native users who value decentralisation and validator diversity over optimal liquidity efficiency would find this design very appealing.

Because yields are still mostly derived from staking incentives, transaction fees, and MEV participation, the protocol's payouts are comparable to more general Ethereum staking returns. However, compared to Lido, Rocket Pool often runs with a lesser liquidity depth, which could result in greater slippage for larger withdrawals.

It is an intentional trade-off. In return for improved decentralisation features and lower validator concentration risk, Rocket Pool forfeits some market efficiency. Validator influence is still more dispersed throughout the network, but users are still exposed to the hazards of liquid staking derivatives and smart contracts.

ether.fi: Liquid Restaking & Yield Stacking

As ether.fi coupled with liquid staking with integrated EigenLayer restaking, it became one of Ethereum's staking platforms with the fastest growth. Through eETH and weETH, ether.fi enables users to access many reward tiers at once, rather than just traditional staking payouts. On ether.fi, users may receive:

- Native Ethereum staking rewards

- EigenLayer incentives

- AVS rewards

- Ecosystem token emissions

- Additional restaking incentives

The same ETH position can produce staking rewards and secure external decentralised systems, which significantly increases capital efficiency.

Higher yields, however, are accompanied by noticeably greater dependency complexity. In addition to Ethereum validator performance, customers of ether.fi are susceptible to governance systems, AVS cutting conditions, EigenLayer infrastructure, smart contract hazards, and cross-protocol contagion.

In addition to creating one of the most intricate risk structures inside Ethereum staking, the protocol basically optimises composability and yield.

EigenLayer: Reusable Economic Security

One of the most significant conceptual shifts in Ethereum staking was brought about by EigenLayer's reusable economic security. EigenLayer enables already staked ETH to protect external systems known as AVSs, or Actively Validated Services, rather than restricting ETH to ensuring Ethereum consensus alone. Included in these systems are:

- Oracle networks

- Middleware infrastructure

- Bridges

- Data availability layers

- Modular blockchain systems

Source: EigenLayer

As a result, ETH became reusable validator collateral that could protect several decentralised systems at once.

While this architecture significantly improves capital efficiency, it also increases interdependence across Ethereum’s staking ecosystem by introducing overlapping validator responsibilities and external slashing exposure.

Source:EigenLayer

Through external validator incentives and AVS participation, EigenLayer generated completely new yield prospects, but it also added linked slashing risk into Ethereum staking. In addition to the Ethereum consensus itself, validators may now be penalised for malfunctions in other infrastructure systems.

As a result, EigenLayer is among Ethereum's most structurally intricate and capital-efficient inventions. Multiple overlapping systems can now be secured simultaneously using the same ETH collateral, enhancing systemic interconnection and dependency exposure while also boosting efficiency.

If you find any issues in this article or notice missing information, please feel free to reach out at team@etherworld.co for clarifications or updates.

To promote your Web3 articles, events, and projects, you may reach out anytime via EtherWorld PR for submissions and collaboration.

Related Articles

- Ethereum Staking Boom Sparks Liquidity & Incentive Debate

- Ethereum Sees Rapid User Growth via New Addresses

- Ethereum Phishing Attack Drains $585K in 11 Hours

- Ethereum Foundation Unstakes 17K ETH Worth $48.9M

- Ethereum Foundation Converts 5,000 ETH to Stablecoins Via CoWSwap

To follow blockchain news, track Ethereum protocol progress, and read our latest stories, subscribe to our weekly today.

Disclaimer: The information contained in this website is for general informational purposes only. The content provided on this website, including articles, blog posts, opinions, & analysis related to blockchain technology & cryptocurrencies, is not intended as financial or investment advice. The website & its content should not be relied upon for making financial decisions. Read full disclaimer & privacy policy.

To stay updated on blockchain news, Ethereum protocol progress, and our latest stories, subscribe to our weekly digest and YouTube channel for ELI5 content.

To promote your Web3 articles, events, project updates, and Press Releases, reach out anytime via EtherWorld PR for submissions and collaboration. For other queries, email contact@etherworld.co.

If you’d like to support our work, share the content and consider donating at avarch.eth.

Join our community on Discord and follow us on Twitter, Facebook, LinkedIn & Instagram.

Author

Nidhi Kumari is a Web3 content writer at EtherWorld.co, tracking ecosystem developments, funding activity, and market trends shaping the crypto space.