CLARITY Act Explained: Inside America’s New Crypto Rulebook

The CLARITY Act could redefine U.S. crypto regulation by creating a clear legal framework for digital assets, exchanges, & institutional adoption.

×

×

Join Our Internship Program

Apply Now →The United States has been struggling with an elementary problem for over ten years: how to control something that didn't exist when your laws were written? Blockchain-based assets and cryptocurrencies have emerged as a distinct category that doesn't cleanly fit under either commodities or securities regulations.

After that, there was a protracted period of ambiguity during which authorities such as the Commodity Futures Trading Commission and the U.S. Securities and Exchange Commission attempted to establish authority, frequently stepping on each other's toes.

This resulted in what many legal professionals have referred to as "regulation by enforcement," a system in which regulations are established through lawsuits and fines rather than being explicitly specified up front. This strategy led to "legal uncertainty, constrained participation of traditional financial institutions, and pushed innovation abroad," according to Arnold & Porter's official advisory.

This structural defect is being addressed by the Digital Asset Market Clarity Act (CLARITY Act). It's about reimagining how new technologies are incorporated into financial systems, not just about cryptocurrency. Its refusal to try to fit cryptocurrency into outdated legal boxes makes it especially significant. Rather, it creates a new framework that accurately depicts how these assets work.

The Act also comes at a time when international regulatory competition is intensifying. If it is unable to provide clarity, the United States runs the risk of lagging behind frameworks like MiCA in Europe and growing experimentation with CBDCs globally. Therefore, the CLARITY Act is about both domestic legislation and global positioning.

- The Current Regulatory Landscape: A System Defined by Conflict

- Key Aspects of the CLARITY Act: A Structured Frameword for Digital Assets

- Defining Digital Assets in Practice: From Issuance to Maturity

- Regulatory Architecture: Who Controls What & Why It Matters?

- Political Dynamics & the Uncertain Path to Law

- Opportunities for Industry: A New Phase of Participation

- From Ambiguity to Architecture

The Current Regulatory Landscape: A System Defined by Conflict

It's crucial to comprehend the environment that the CLARITY Act is attempting to improve before delving into its real proposals. Instead of developing through a defined legislative blueprint, the U.S. crypto regulatory structure has been shaped by regulators' continuous disagreements and conflicting power.

The Commodity Futures Trading Commission and the U.S. Securities and Exchange Commission are at the core of this conflict. The two organisations have essentially different approaches to digital assets. The SEC typically treats most tokens as securities linked to investment contracts by applying the Howey Test. Conversely, the CFTC has continuously favoured categorising more decentralised assets as commodities.

Although this discrepancy in interpretation may seem like a technical policy dispute, it actually produces a very unpredictable situation. When they introduce tokens, startups frequently aren't sure which regulatory framework they are operating under.

Exchanges list assets while managing the possibility that they may be reclassified in the future. Depending on how a token is defined at any given time, even investors are left vulnerable to inconsistent protections.

This is further complicated by the fact that the system has mostly developed through court rulings and enforcement actions rather than being governed by explicit regulations. Therefore, clarity frequently follows conflict rather than precedes it.

In this case, the underlying pattern is crucial. For both institutional investors and builders, any clarification of regulations, even in specialised markets like stablecoins, is instantly interpreted favourably. Conversely, involvement decreases when there is a lack of clarity.

That's actually the main problem. The technology has advanced, the use cases are growing, and the cash is there, but the system finds it difficult to proceed with confidence in the absence of a stable regulatory framework.

This precise gap is filled by the CLARITY Act, which seeks to replace conflict-driven interpretation with a framework that is established beforehand rather than after the event.

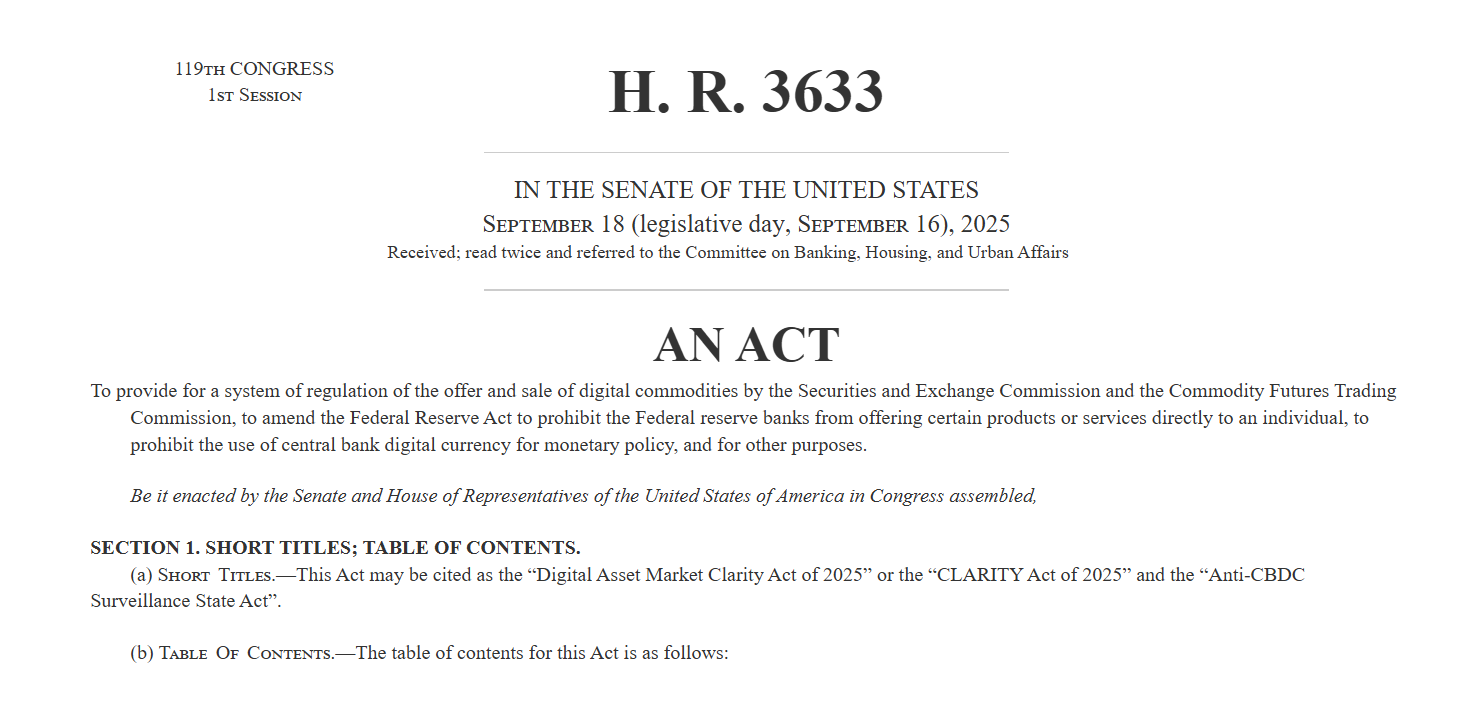

Source: US Senate Committee

Key Aspects of the CLARITY Act: A Structured Frameword for Digital Assets

Fundamentally, the CLARITY Act aims to close one of the largest gaps in the cryptocurrency industry, i.e., there has never been a precise definition of what certain digital assets are. The Act adopts a more pragmatic approach rather than classifying everything into a single group. It acknowledges that different tokens have different functions and should not be handled equally as a result.

Some tokens are intended to serve as payment tools, while others are used to manage and support blockchain networks. Still others are made only to raise money. The CLARITY Act bases its structure on these distinctions, establishing distinct categories to ensure that regulations really reflect the real-world uses of these assets.

This method is unique in that it does not regard tokens as static objects. A project may start as a small group of founders soliciting money, but it may eventually develop into a decentralised network with no single organisation in charge.

As the network develops, the Act recognises this change and permits a token to transition between different categories. This adaptability is crucial because it mirrors the real growth of the cryptocurrency ecosystem.

Simultaneously, the Act provides accountability where it counts most-early on. It is expected of projects to be open and honest about how their system functions, how tokens are allocated, and what users are entering into.

Overall, the framework seems to be more about creating regulations based on how cryptocurrency actually functions today than it is about forcing it into outdated regulations.

Source: CLARITY Act

Defining Digital Assets in Practice: From Issuance to Maturity

One of the most intelligent aspects of the CLARITY Act is the way it considers a token over its whole existence, not only at the time of introduction. The majority of cryptocurrency initiatives actually don't begin as decentralised.

Generally, they start with a core team that holds a significant portion of tokens, builds the protocol, and raises money. At that point, it is evident that the token shares traits with an investment because it is linked to the actions and choices of a certain group.

Rather than attempting to refute this starting point, the Act accepts it. However, it acknowledges that this position is not static. Control tends to spread among developers, consumers, and validators as a network expands. The initial team's influence steadily diminishes as decision-making gets increasingly spread. By adding the concept of a "mature" blockchain system, the CLARITY Act expands upon this shift.

A network must satisfy specific quantifiable requirements in order to be deemed mature. For instance, no single entity should possess a disproportionate number of tokens; typically stated criteria are approximately 20% ownership or control. In order to eliminate reliance on a single central authority, the network should also function transparently, using open-source programming and publicly verifiable regulations.

This modification affects how the asset is seen, which makes it significant. Over time, a token that at once appeared to be an investment linked to a team may begin to act more like a network commodity, something that people use rather than invest in for managerial returns.

In this case, the CLARITY Act is very useful. At launch, a token's identity is not frozen. Rather, it makes it possible for regulations to change in tandem with technology, something that previous frameworks were just not built to handle.

Regulatory Architecture: Who Controls What & Why It Matters?

The CLARITY Act aims to address both the definition of digital assets and the issue of who has the authority to govern them. There is currently a lot of confusion because that responsibility is unclear. Based on how an asset truly operates, the Act seeks to establish a more distinct boundary between the Commodity Futures Trading Commission and the U.S. Securities and Exchange Commission.

To put it simply, a token is subject to the SEC, much like traditional securities, if it is being used to generate capital from investors and is linked to the work of a particular team.

However, regulatory authority switches to the CFTC, which deals with commodities like Bitcoin, as that same network becomes more decentralised and the token begins to operate independently as part of a larger ecosystem.

This change has actual repercussions; it is not only symbolic. Particularly when it comes to fundraising, the SEC usually enforces more stringent disclosure and compliance rules.

In contrast, the CFTC is primarily concerned with trading activities, market integrity, and stopping commodity market manipulation. Therefore, the regulatory burden and the types of protections that are applicable depend on where a token is located.

The CLARITY Act clearly places spot markets for digital commodities under supervision, which is another significant move. Up until recently, the CFTC's power has been comparatively restricted in spot trading but more robust in futures markets. The Act broadens that reach, requiring cryptocurrency exchanges that deal in these assets to register and adhere to specific regulations.

This results in a system where responsibilities no longer overlap, at least in theory. Each has a specific function, as opposed to two regulators tugging in opposite directions. And because understanding who governs you is frequently the first step towards understanding how to comply, that clarity might have a big impact on the sector.

Political Dynamics & the Uncertain Path to Law

Although the CLARITY Act appears to be well-structured on paper, it has not been easy to navigate the American political system. With bipartisan support, it passed the House of Representatives in 2025, which is noteworthy considering how polarised American policymaking is typically. However, because crypto regulation lies at the nexus of technology, finance, and political risk, its passage through the Senate has been slower.

One of the primary points of contention is the relative authority of the Commodity Futures Trading Commission and the U.S. Securities and Exchange Commission.

Given that the CFTC has historically been a smaller organisation, some legislators are not entirely persuaded that giving it more supervision is the proper course of action. For comparison, the CFTC operates with about $400–500 million, but the SEC has an annual budget of over $2 billion. This raises practical questions about whether the CFTC can manage an enlarged role in retail cryptocurrency markets.

Stablecoins are also a topic of continuous discussion, especially in light of their expanding use in trading and payments, and whether more security measures are necessary.

These distinctions do not necessarily indicate that the Act will fail, but they do account for the slow pace of advancement. However, all sides concur that structural control of some kind is unavoidable because the current system is ineffective.

Opportunities for Industry: A New Phase of Participation

The most significant change will not only be legal but also behavioural if the CLARITY Act proceeds in its current form. Large financial institutions have been wary of cryptocurrency for years, not because there was no opportunity, but rather because the regulatory risk was too uncertain.

It becomes challenging to defend significant capital allocation when you don't know whether regulations apply or whether they might be altered after the fact.

That dynamic is almost instantly altered by clarity. A variation of this has previously occurred in the marketplace. Institutional inflows into crypto-linked funds exceeded $10 billion in a comparatively short amount of time following stronger regulatory signals regarding spot Bitcoin products in the U.S., demonstrating how rapidly confidence may return when the rules are properly established.

The same reasoning holds more generally; when compliance becomes predictable, participation tends to rise among asset managers, banks, and fintech companies.

The Act may also spur expansion in fields such as tokenisation, which is the representation of conventional assets on blockchain networks, such as government securities, real estate, or private stock. These concepts are currently undergoing large-scale testing; thus, they are no longer experimental. However, most big businesses are reluctant to proceed past pilot stages in the absence of a clear regulatory framework.

That hesitancy is lessened by the CLARITY Act. Although it does not eliminate risk, it does make the boundaries apparent. And in the financial markets, it in and of itself may be sufficient to change behaviour from passive observation to active involvement.

From Ambiguity to Architecture

More broadly, the CLARITY Act signifies the shift from an uncertain to a structured system. Up until now, court rulings and enforcement actions have played a major role in the development of crypto regulation in the United States. This implies that insight frequently doesn't emerge until something goes wrong.

The Act aims to change that trend by establishing a clear structure right away. It assigns regulatory authority, creates more precise classifications, and, most importantly, acknowledges that digital assets change over time. The final criterion is crucial because, in a field that evolves as swiftly as cryptocurrency, a system that is unable to adapt to change will soon become obsolete.

This does not imply that every issue will be fully handled. The framework will probably need to be modified as new use cases arise, and there will still be ambiguities. However, it is a significant change to go from a situation where the rules are ambiguous to one where they are at least structured.

The CLARITY Act is essentially about laying a foundation. Markets expand on confidence as much as invention. Additionally, people gain confidence when they comprehend the system they are working in. The Act makes it feasible by substituting a more defined infrastructure for uncertainty.

If you find any issues in this article or notice missing information, please feel free to reach out at team@etherworld.co for clarifications or updates.

To promote your Web3 articles, events, and projects, you may reach out anytime via EtherWorld PR for submissions and collaboration.

Related Articles

- SEC Redraws Crypto Boundaries in Major Policy Shift

- Mastercard Launches Crypto Partner Program for Global Payments

- US Banking Regulators Clarify Capital Treatment for Tokenized Securities

- IRS Proposes Digital Tax Forms for Crypto Traders

- CFTC Chair Says U.S. Crypto Clarity Bill Closer Than Ever

To follow blockchain news, track Ethereum protocol progress, and read our latest stories, subscribe to our weekly today.

Disclaimer: The information contained in this website is for general informational purposes only. The content provided on this website, including articles, blog posts, opinions, & analysis related to blockchain technology & cryptocurrencies, is not intended as financial or investment advice. The website & its content should not be relied upon for making financial decisions. Read full disclaimer & privacy policy.

To stay updated on blockchain news, Ethereum protocol progress, and our latest stories, subscribe to our weekly digest and YouTube channel for ELI5 content.

To promote your Web3 articles, events, project updates, and Press Releases, reach out anytime via EtherWorld PR for submissions and collaboration. For other queries, email contact@etherworld.co.

If you’d like to support our work, share the content and consider donating at avarch.eth.

Join our community on Discord and follow us on Twitter, Facebook, LinkedIn & Instagram.

Author

Nidhi Kumari is a Web3 content writer at EtherWorld.co, tracking ecosystem developments, funding activity, and market trends shaping the crypto space.