50+ Global Banks Back SWIFT’s Shift Toward Ethereum

SWIFT upgrades global payments with 50+ banks while building an Ethereum-based layer for real-time cross-border settlement.

SWIFT published that Fifty-plus banks spanning six continents have signed onto a new payments framework, with more than 25 committed to going live by June 2026. The corridors cover eleven countries including Australia, Bangladesh, Canada, China, Germany, India, Pakistan, Spain, Thailand, the UK and the US. And sitting quietly alongside it is a parallel initiative built on Ethereum which could change what cross-border settlement means at the institutional scale.

- The Framework and What It Fixes

- The Banks Behind It

- The Ethereum Layer Nobody Is Talking About

- Why Both Tracks Matter

The Framework and What It Fixes

Cross-border payments have a well-known reputation problem. The fees are unpredictable, the timelines are not very clear and the experience for someone receiving a remittance in Dhaka or Mumbai has historically been far worse than for someone wiring money between two banks in the same city. SWIFT's messaging network was never really the problem, 75% of transactions across it already reach the destination bank within ten minutes, which is ahead of the G20's own targets. The delay has always been what happens after.

📢 BREAKING: SWIFT confirms 25+ banks going live by June, settling on Ethereum for 24/7 cross-border payments. 🚀

— Ethprofit.eth 🦇🔊 (@Ethprofit) March 23, 2026

Source: https://t.co/WzfGKoveKm pic.twitter.com/Fe3loWHa2c

The gap between a payment arriving at a recipient bank and the money appearing in a customer's account, accounts for roughly 80% of a transaction's total journey time. Local regulations, domestic infrastructure limitations, and individual bank practices all contribute to delays that SWIFT's messaging layer has no control over. The new Swift Payments Scheme changes that by enforcing commitments on exactly this part of the journey: fixed costs disclosed upfront, full value delivered to the recipient, end-to-end traceability and the fastest possible settlement including instant where local infrastructure allows.

Five of the eleven launch markets, Bangladesh, China, Germany, India and Pakistan are among the ten largest remittance-receiving countries in the world. The people who stand to benefit most from cost certainty and predictable delivery are precisely the ones sending and receiving money across these corridors.

The Banks Behind It

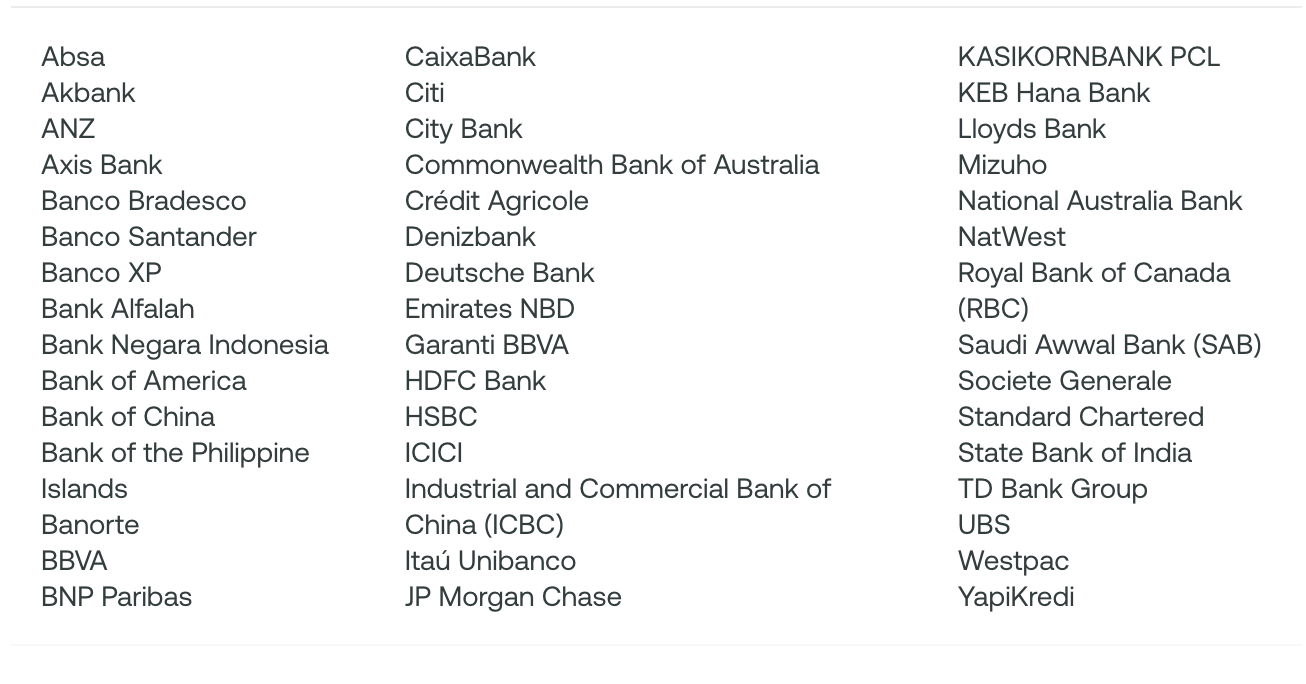

The list of institutions supporting this framework reads like a roll call of global banking. Bank of America, JP Morgan Chase, HSBC, Citi, Deutsche Bank, BNP Paribas, Standard Chartered, Santander, BBVA, Lloyds, NatWest, State Bank of India, HDFC Bank, ICICI, ANZ, Westpac, Commonwealth Bank of Australia, Royal Bank of Canada, UBS, Mizuho, Société Générale, Crédit Agricole, and more, over 50 institutions in total, with the initial 25-plus going live by June covering the launch corridors.

When institutions of this weight align on a common set of rules, the practical effect on how cross-border payments work is substantial regardless of the technology underneath. This is SWIFT doing what it has always done best but applying that muscle to the retail and SME segment that has historically received the most inconsistent experience.

This directly serves the G20's roadmap for cross-border payments, which sets targets across speed, cost, transparency, access and choice to be met by 2027. The framework is one of the more concrete steps toward those targets that the financial community has taken.

The Ethereum Layer Nobody Is Talking About

Running in parallel and SWIFT is deliberate about calling these two separate tracks, is a blockchain-based shared ledger that SWIFT is adding to its infrastructure stack. The technical partner is ConsenSys. The network is Linea, the zero-knowledge Ethereum Layer 2 that ConsenSys developed.

Linea is a zk-EVM, it executes smart contracts in a way that is fully compatible with Ethereum's tooling but settles transactions through zero-knowledge proofs, making it significantly more efficient and cost-effective than Ethereum mainnet for high-volume institutional use. SWIFT is not connecting to public Ethereum directly; it is using Linea as the execution layer, which inherits Ethereum's security model while being practically suited to the scale and compliance requirements of a network serving 11,500 institutions across more than 200 countries.

The purpose of the shared ledger is to enable 24/7 real-time cross-border settlement of regulated tokenised value across SWIFT's existing institutional network. More than 30 banks are involved in developing this, including BNP Paribas, BNY Mellon and several institutions that also appear in the payments scheme. Earlier pilots in 2025 tested tokenised bond settlement and stablecoin flows through Linea, with results that shaped the current prototype.

This is still in development. It does not have a confirmed go-live date tied to June. SWIFT is building a path for regulated tokenised value to move on-chain through Ethereum infrastructure, inside the most systemically important financial messaging network in the world.

Why Both Tracks Matter

The two initiatives serve different timelines. The payments scheme delivers a better version of what the banking system already does and it does so immediately, for real people sending money home across eleven countries by mid-2026. The Linea ledger is the longer play, positioning SWIFT to be the trusted interoperability layer for tokenised finance when that market matures.

Running both simultaneously is the significant strategic point. SWIFT does not have to bet on a single timeline for when tokenised finance becomes the norm. It participates in the present with the payments scheme and in the future with the blockchain layer, connecting the two when the conditions are ready. For institutions that have spent years watching DLT pilots stall, this parallel approach offers a practical path forward that does not require abandoning the infrastructure they already rely on.

For the Ethereum ecosystem, ConsenSys building the technical layer for SWIFT's on-chain ambitions places Linea, and by extension Ethereum's security model inside the infrastructure that connects global banking. That is not a consumer adoption story. It is an infrastructure story, and those tend to matter more permanently.

If you find any issues in this article or notice missing information, please feel free to reach out at team@etherworld.co for clarifications or updates.

To promote your Web3 articles, events, and projects, you may reach out anytime via EtherWorld PR for submissions and collaboration.

Related Articles

- An Introduction to Ethereum’s DAO-Funded Security Model

- Ethereum Foundation's First-Ever Treasury Policy Explained

- Ethereum has Deployed Another $7.6M Into Morpho! Here's Why

- After CoinDCX: Where Should Indian Crypto Users Actually Trade?

- CoinDCX Founders Questioned in Fraud Case, Company Blames Impersonation Scam

To follow blockchain news, track Ethereum protocol progress, and read our latest stories, subscribe to our weekly today.

Disclaimer: The information contained in this website is for general informational purposes only. The content provided on this website, including articles, blog posts, opinions, & analysis related to blockchain technology & cryptocurrencies, is not intended as financial or investment advice. The website & its content should not be relied upon for making financial decisions. Read full disclaimer & privacy policy.

To stay updated on blockchain news, Ethereum protocol progress, and our latest stories, subscribe to our weekly digest and YouTube channel for ELI5 content.

To promote your Web3 articles, events, project updates, and Press Releases, reach out anytime via EtherWorld PR for submissions and collaboration. For other queries, email contact@etherworld.co.

If you’d like to support our work, share the content and consider donating at avarch.eth.

Join our community on Discord and follow us on Twitter, Facebook, LinkedIn & Instagram.