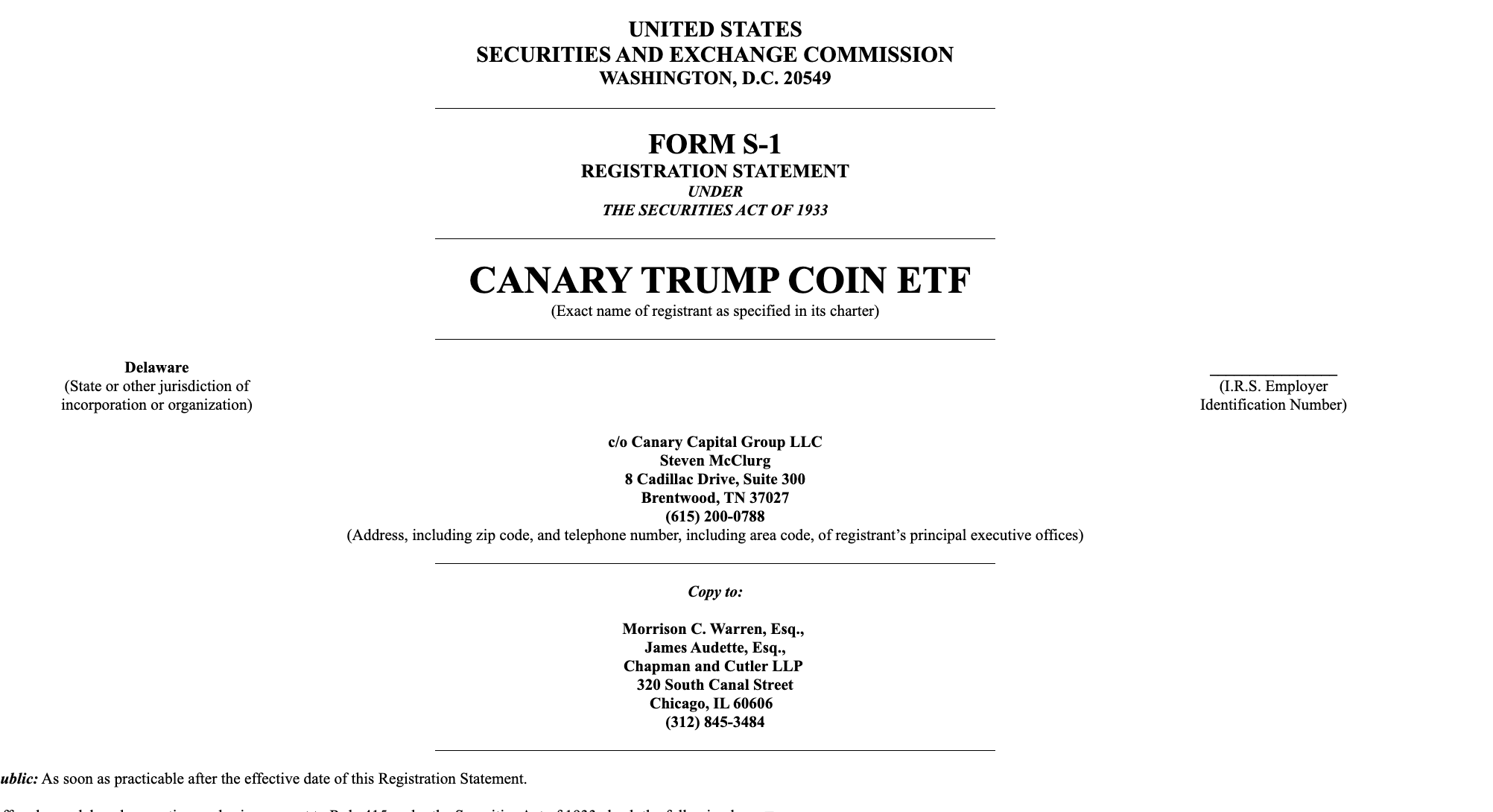

Canary Capital Files SEC Application for $TRUMP Token Fund

Canary Capital submitted an S-1 seeking SEC approval for an exchange‑traded fund tied to the $TRUMP token.

Canary Capital has submitted an S-1 registration statement to the U.S. Securities and Exchange Commission (SEC) seeking approval to launch an exchange-traded product (ETP) tied to the digital asset known as $TRUMP.

The filing is an S-1 registration and would also require a separate exchange rule change (Form 19b-4) before any shares could list. Given questions about market surveillance, token classification, custody support, and index quality, approval is uncertain and timelines are likely extended. The proposed product is not affiliated with any political campaign or public figure.

An exchange-traded product trades on stock exchanges in the same way as a stock. Instead of purchasing the token directly through a crypto platform, investors would be able to buy shares of the fund through a brokerage account. The fund is designed to track the price of $TRUMP, though details such as custody arrangements, pricing methodology, fees and the listing venue are not yet disclosed.

The SEC’s review will consider several gating issues. Spot crypto approvals to date, such as Bitcoin and Ether, have relied on large, surveilled markets and surveillance-sharing agreements. In contrast, trading activity for smaller tokens is often concentrated on offshore exchanges or decentralized venues, raising questions about whether they meet the SEC’s Market of Significant Size (MoSS) and manipulation-resistance standards.

Another key factor is classification. If $TRUMP is deemed a security, the disclosure, custody and distribution requirements become significantly more complex. Custody is also central: approval depends on whether regulated custodians support the token at scale with SOC-audited controls and incident-response frameworks. Pricing benchmarks will matter as well, since indexes pulling from thin or illiquid venues can increase tracking error.

Canary Capital has been active with multiple filings, including an “American-Made” basket of U.S.-associated tokens and other single-asset products. Together, these applications suggest a strategy of packaging niche digital assets into structures familiar to traditional investors.

If the SEC advances the filing, future amendments are expected to outline creation/redemption mechanics (likely cash-only), pricing benchmarks, custody partners, fees, and the proposed exchange. For now, the S-1 highlights a new attempt to bridge speculative tokens and regulated markets, though the outcome will depend on how regulators weigh surveillance, classification, custody, and investor-protection concerns.

Recomended Articles

- SEC Says "Liquid Staking Tokens Are Not Securities"

- Breaking: SEC Stops Treating Crypto Devs Like Criminals - What are the New Rules?

- Polygon’s POL Staking: Unlock Rewards, Airdrops and the AggLayer

- Linea Launches ETH Burn, Yield Rewards & Ecosystem Fund

- MetaMask’s “Stablecoin Earn” Goes Live with Aave

Disclaimer: The information contained in this website is for general informational purposes only. The content provided on this website, including articles, blog posts, opinions, and analysis related to blockchain technology and cryptocurrencies, is not intended as financial or investment advice. The website and its content should not be relied upon for making financial decisions. Read full disclaimer and privacy Policy.

For Press Releases, project updates and guest posts publishing with us, email to contact@etherworld.co.

Subscribe to EtherWorld YouTube channel for ELI5 content.

Share if you like the content. Donate at avarch.eth

You've something to share with the blockchain community, join us on Discord!