Catch-22 for unbanked: how can billion people find the way to the global economy

By Anton Dzyatkovsky, co-founder of MicroMoney

The catch-22 is a paradoxical situation from which an individual cannot escape because of contradictory rules. The catch-22 of modern banking is that if you need a credit, you need a credit score, and to get a credit score you need a credit. Logically enough, banks have to spend hundreds of dollars to scrutinize potential client’s creditworthiness. For example, in US banks pay $200–300 of operational costs, in Asia - $100–150 for one loan approved, and wasting money is not what they want. People who can not escape the endless circle “credit vs credit score” are called “unbanked.”

According to the McKinsey, two billion individuals and 200 million micro, small, and midsize businesses on emerging markets today lack access to savings and lending service, and even those with the access have a limited range of financial products.

It's not like banks do not put efforts to assess the unbanked client's creditworthiness at all. Many financial companies learned to use alternative ways to explore it. For example, in the UK a bank during mortgage availability assessment can examine all of your purchases and check-ins in pubs within the year to determine your alcohol expenses. In Mexico, Banco Azteca sends its agents to the homes of borrowers to take an inventory of stereos, TVs and other appliances they possess to support their loan application. Sesame Credit, a rating company, ran by Alibaba, sees over 400m active users a month and relies on users’ online-shopping habits to calculate their credit scores. These observations lead to the conclusion that someone playing video games for ten hours a day might be rated a bad risk; a frequent buyer of nappies would be thought more responsible. Therefore, any software solutions that can accumulate and analyze information from all these additional sources are predictable for fintech market.

McKinsey used its proprietary general equilibrium macroeconomic model and detailed inputs from field research in seven emerging economies that cover a range of geographies and income levels: Brazil, China, Ethiopia, India, Mexico, Nigeria, and Pakistan. Agency reported that some 1.6 billion unbanked people could gain access to formal financial services; of this total, more than half would be women. $2.1 trillion of loans to individuals and small businesses could be made sustainably, as providers expand their deposit bases and have a newfound ability to assess credit risk for a wider pool of borrowers.

Rather than waiting for a billion people’s incomes to rise and traditional financial institutes to extend their reach, emerging economies have an opportunity to use mobile technologies to provide digital financial services for all, rapidly unlocking economic opportunity and accelerating social development.

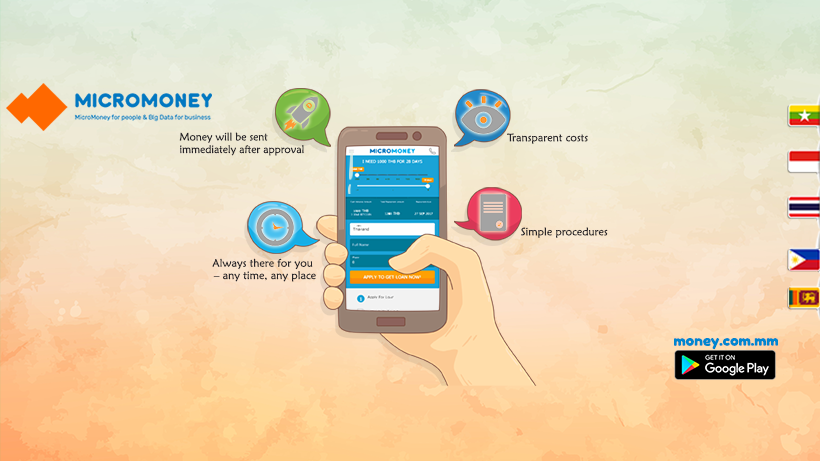

Access to the payday loan, fast, paperless, with an affordable interest rate is what makes our company, MicroMoney, the solution for financial catch-22. MicroMoney, is a global digital credit bureau based on the blockchain technology. The company gives an opportunity for unbanked people to start from a blank slate meaning their empty credit histories. It also creates the way for banks, retail, and insurance companies to reduce financial risks when they work with this untapped audience.

In what way? MicroMoney has developed a mobile scoring system for rapid assessment of a client’s creditworthiness. Relying on Big Data, neural networks, and machine learning it has the functionality to approve the very first loans for unbanked people and this way creates their credit histories from scratch a hundred times cheaper than traditional banks. At the same time, financial and other companies get the access to this credit rating database on a fee basis, allowing them to receive a list of reliable and already assessed customers ready to consume their offers.

Now in our company and, I hope, everywhere in the nearest future, the unbanked person doesn’t need to collect a number of paper-based documents to confirm the ability to repay. He or she is just installing the MicroMoney mobile app on a smartphone and completing a loan application within it. Then the scoring self-learning system analyzes the data available from the borrower's smartphone and identifies potential credit risks with an accuracy of more than 95%. In a few minutes program makes a decision whether a loan should be approved or not, and sends money to a customer’s e-wallet if the answer is yes.

Our company processed more than 95,000 unique customers already and got more than 500,000 likes on Facebook during the first two years of work. Nine customers out of ten took the first loan in their lives, and 73% of these people came back for a new one.

Aspiring to growth and development, we are preparing to launch a token distribution campaign to carry out the business plan of shaping the legal market for creating and maintaining credit histories from scratch. Billions of unbanked people are ready to be the part of the global economy, want to improve their lives, and the access to financial services gives them this opportunity.

Now MicroMoney operates in Thailand, Cambodia, Indonesia, Sri-Lanka, and Myanmar and we have the ambitious plans to enter five more emerging markets in the nearest months, including Nigeria and the Philippines. A token distribution campaign will start on 18th of October to support these business plans and to involve new streams of money from the untapped audience to the global economy.

Learn more about MicroMoney at

-

Website: https://micromoney.io/

-

White paper: https://micromoney.io/MicroMoney_whitepaper_ENG.pdf

-

Twitter: @micromoneyio

-

Facebook: @micromoneymyanmar

-

Telegram: https://t.me/micromoneyico

-

Media Contact

*Name: Olga Rusakova

*Email: orusakova@micromoney.io

*Company: MicroMoney

Disclaimer: This is a sponsored article and should NOT be viewed as an endorsement by EtherWorld. Readers are requested to do their own research before investing into any project.

For more updates, technical blogs and general discussion on blockchain technology & Ethereum, please join us at Website, Reddit, Facebook, Medium, Steemit and Twitter. Feel free to email your suggestions.