India’s Crypto TDS Crosses ₹511 Crore in FY25

India’s crypto TDS surged to ₹511.83 crore in FY 2024-25 as trading activity concentrated in Maharashtra & Karnataka, revealing rising compliance, exchange level dominance, & key policy questions ahead.

India’s crypto taxation framework is beginning to tell a clearer story through hard numbers. Official data presented in Parliament shows that TDS collected from crypto transactions reached ₹511.83 crore in FY 2024 25, marking a sharp 41 percent increase over the previous year.

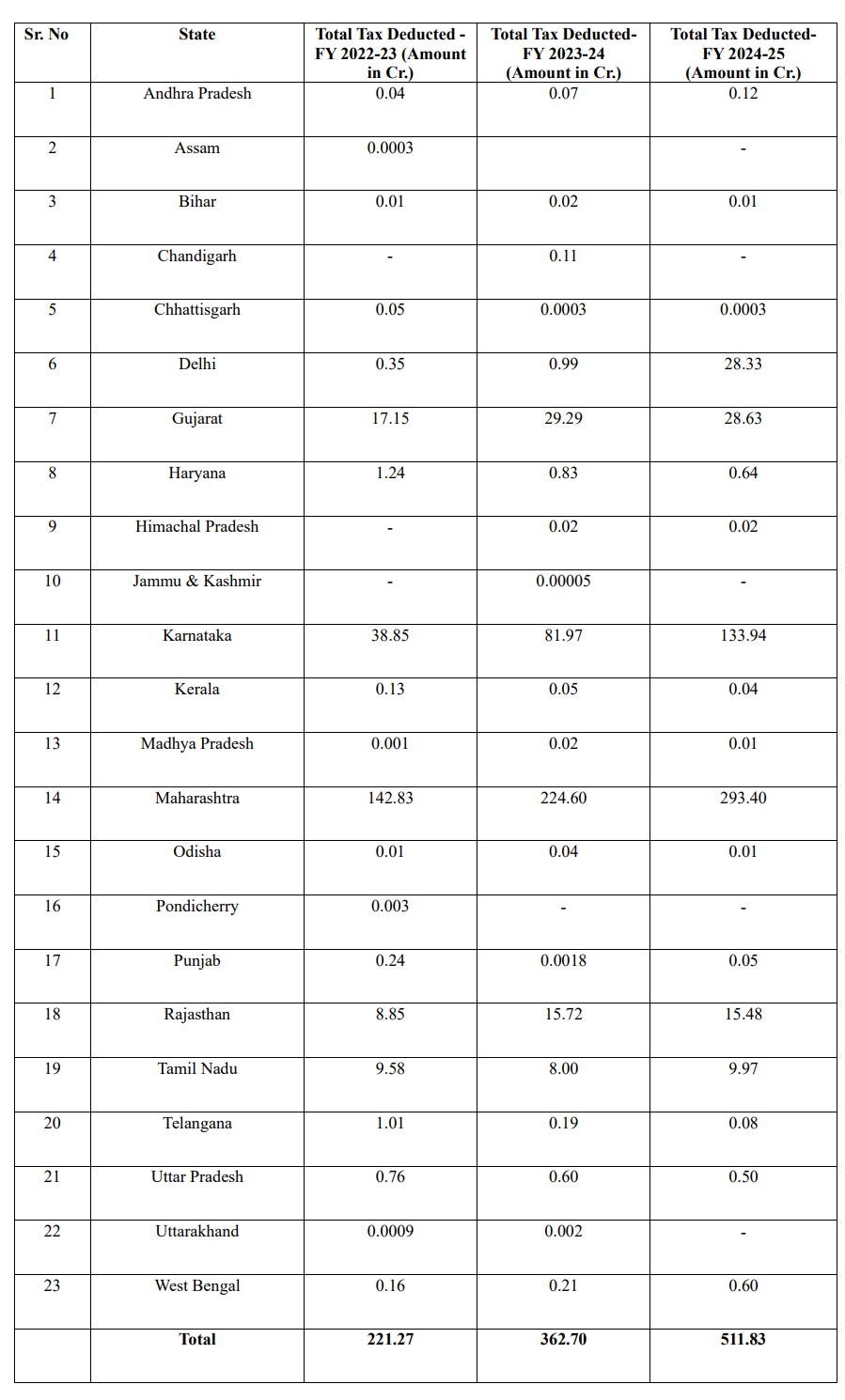

Just two years ago, total collections stood at ₹221.27 crore, underscoring how quickly the tax footprint of crypto activity has expanded in the country. The data, released by the Ministry of Finance in response to a Lok Sabha question on crypto currency taxation, provides a rare state wise breakdown of TDS collections over the last three financial years.

Beyond headline growth, it reveals deeper structural shifts in where crypto trading is concentrated, how compliance is evolving, & which exchanges appear to be carrying the bulk of the tax burden.

- Crypto TDS Growth, A Three Year Snapshot

- CoinDCX & the Rise of Exchange Level Concentration

- Government Enforcement & Non Compliance Concerns

- The Bigger Policy Question, What Comes Next

Crypto TDS Growth, A Three Year Snapshot

India introduced a 1 percent TDS on crypto transactions under Section 194S of the Income Tax Act as part of the Finance Act 2022. The move was designed to create traceability & ensure tax reporting rather than to raise revenue directly.

Three years later, the revenue trail is becoming increasingly visible. According to the Finance Ministry:

- FY 2022-23: ₹221.27 crore

- FY 2023-24: ₹362.70 crore

- FY 2024-25: ₹511.83 crore

The year on year rise suggests that crypto trading has not disappeared under the tax regime, as many feared initially. Instead, a substantial volume of activity continues to flow through platforms where TDS is deducted & deposited with the government.

However, officials have also clarified that these numbers do not capture the entire crypto market. They only reflect transactions routed through compliant entities. Activity on offshore platforms that do not deduct TDS may still remain partially outside this dataset.

One of the most striking aspects of the parliamentary disclosure is the uneven geographic distribution of crypto TDS collections. In FY 2024 25, just a handful of states account for the overwhelming majority of collections:

- Maharashtra: ₹293.40 crore

- Karnataka: ₹133.94 crore

- Gujarat: ₹28.63 crore

- Delhi: ₹28.33 crore

- Rajasthan: ₹15.48 crore

- Tamil Nadu: ₹9.97 crore

By contrast, many states report collections below ₹1 crore, with some registering near zero values across multiple years. This imbalance does not necessarily imply that crypto usage is absent in smaller states.

Source: sansad.in

Instead, it points to how crypto trading activity that generates large taxable volumes is clustered around specific hubs. It also reflects where major exchanges operate, where high value traders are located, & how deductor level reporting maps activity to states.

Delhi’s numbers are particularly notable. From less than ₹1 crore in FY 2023 24, collections jumped to over ₹28 crore in FY 2024 25, suggesting a sharp shift in where compliant trading activity is being recorded.

Maharashtra alone contributed more than half of India’s total crypto TDS in FY 2024-25. Karnataka added another large share, together forming the core of India’s crypto tax base.

There are several reasons why this concentration is logical.

- First, Maharashtra is home to Mumbai, India’s financial capital. Large proprietary traders, high net worth individuals, & institutional style crypto participants are more likely to be based there.

- Second, Karnataka, particularly Bengaluru, has emerged as India’s crypto & fintech nerve centre. Many exchanges, blockchain startups, & technology teams operate from the state, creating a natural clustering of high frequency & high volume trading.

- Third, compliance infrastructure tends to consolidate where professional operations exist. Exchanges with strong legal, tax, & reporting capabilities are more likely to ensure accurate TDS deduction & timely deposit, which then reflects in state wise numbers.

CoinDCX & the Rise of Exchange Level Concentration

Alongside state level concentration, exchange level concentration is also becoming visible. CoinDCX has publicly stated that it deposited ₹259.58 crore in TDS during FY 2024 25, amounting to roughly half of India’s total crypto TDS collection for the year.

The Total TDS deposited by CoinDCX during FY 24-25 is Rs. 259.58 Cr.

— Sumit Gupta (CoinDCX) (@smtgpt) December 26, 2025

So CoinDCX paid around 50% of total tds. https://t.co/PQkNhGrcbK

This single data point highlights a broader trend. A small number of large, compliant exchanges appear to be responsible for most of the tax flow to the government, while a fragmented long tail of platforms contributes relatively little.

For policymakers, this creates both reassurance & risk.

- On one hand, it shows that enforcement works when platforms are regulated & monitored.

- On the other, it raises questions about market concentration & whether current tax rules unintentionally favour a few large players.

Government Enforcement & Non Compliance Concerns

The Finance Ministry has acknowledged that compliance is not universal. According to the parliamentary reply, survey actions under Section 133A of the Income Tax Act were conducted against three crypto exchanges. These actions uncovered:

- ₹39.8 crore in unpaid TDS

- ₹125.79 crore in undisclosed income at the exchange level

- ₹888.82 crore in undisclosed income linked to virtual digital asset transactions across broader investigations

Officials also noted that certain offshore crypto platforms serving Indian users are not complying with TDS provisions, despite the law applying to them if income is chargeable to tax in India.

All Virtual Asset Service Providers catering to Indian users are required to register with FIU IND under PMLA, strengthening the government’s ability to monitor flows from an AML & compliance standpoint.

The rising TDS figures challenge the narrative that India’s crypto market has collapsed under taxation. Instead, they suggest a market that has adapted. Key signals emerging from the data include:

- Trading activity is consolidating rather than disappearing

- High volume traders continue operating within compliant frameworks

- Government visibility into crypto flows is improving year by year

- Regional & platform level concentration is increasing

At the same time, the data also reinforces concerns that the 1 percent TDS creates friction for smaller traders & may still be pushing some activity offshore.

The Bigger Policy Question, What Comes Next

The Finance Ministry has clarified that it has not conducted studies on alternative crypto taxation models used in countries like Thailand or Indonesia. For now, India appears committed to its existing framework.

As TDS collections continue to rise, the debate is shifting. The question is no longer whether crypto trading exists in India. It is whether the current tax design can support a balanced, competitive market without excessive concentration or leakage.

With over ₹500 crore now flowing annually through crypto TDS alone, digital assets are firmly part of India’s fiscal reality. How policymakers choose to refine the system next will determine whether this market evolves sustainably or remains tightly constrained within a narrow corridor of compliance.

If you find any issues in this blog or notice any missing information, please feel free to reach out at yash@etherworld.co for clarifications or updates.

Related Articles

Disclaimer: The information contained in this website is for general informational purposes only. The content provided on this website, including articles, blog posts, opinions, & analysis related to blockchain technology & cryptocurrencies, is not intended as financial or investment advice. The website & its content should not be relied upon for making financial decisions. Read full disclaimer & privacy policy.

For Press Releases, project updates & guest posts publishing with us, email contact@etherworld.co.

Subscribe to EtherWorld YouTube channel for ELI5 content.

Share if you like the content. Donate at avarch.eth.

You've something to share with the blockchain community, join us on Discord!

Author

Blockchain Content & Ops Specialist, Avarch LLC.