Indian MP Raghav Chadha Introduces Asset Tokenisation Bill 2026

Indian MP Raghav Chadha introduces the Asset Tokenisation (Regulation) Bill, 2026 to create a legal framework for tokenised real-world assets in India.

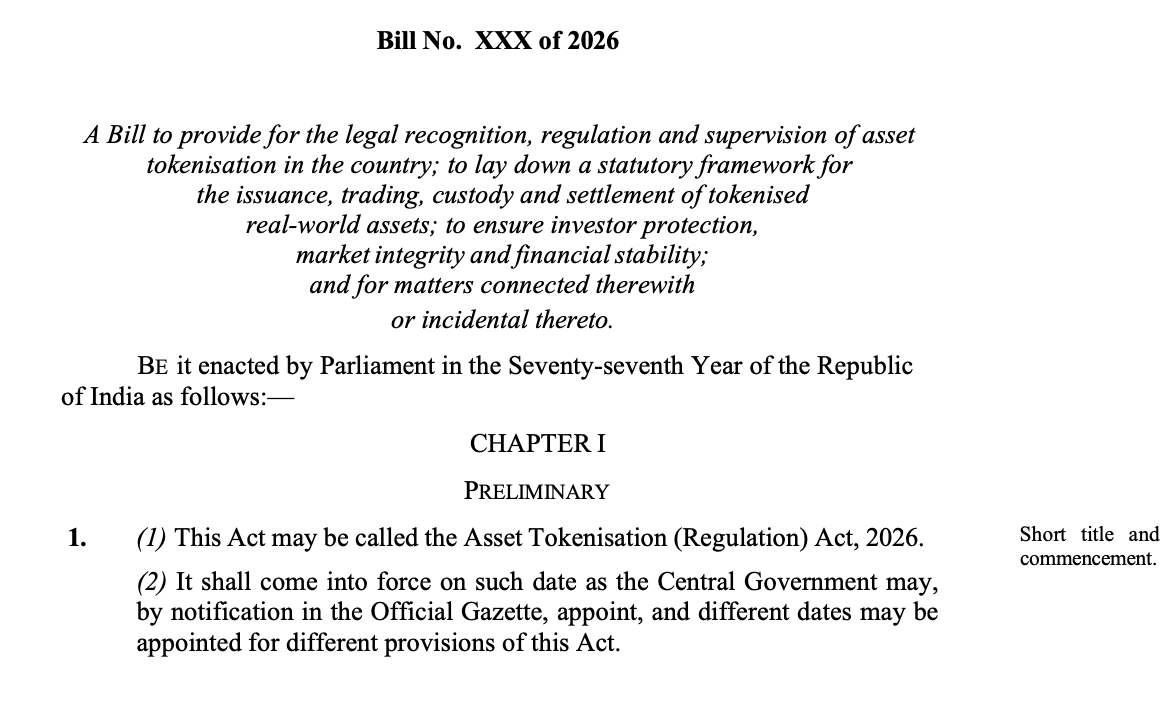

India may be inching closer to a formal legal framework for tokenised real-world assets after Member of Parliament Raghav Chadha introduced The Asset Tokenisation (Regulation) Bill, 2026 in Parliament.

At a time when global financial institutions are increasingly exploring tokenisation for bonds, funds, real estate, commodities, receivables, & other assets, the proposed bill signals that India is beginning to engage with the subject not just as a technology trend, but as a policy issue that may eventually require dedicated law.

Across jurisdictions, financial players are experimenting with putting treasury products, money market instruments, real estate fractions, private credit, carbon assets, & other forms of value on digital rails. India, however, still lacks a dedicated statute addressing this space.

The new Private Member Bill attempts to change that by proposing a structured legal architecture for issuance, trading, custody, settlement, supervision, audits, penalties, & appeals for tokenised real-world assets.

- What the Bill Actually Covers

- Who Would Regulate Tokenised Assets?

- Why This Could Be Important for India’s Digital Finance Future

Its stated objective is to establish a comprehensive legal & regulatory framework for the issuance, trading, custody, & supervision of tokenised real-world assets in the country. The proposal also notes that current legal uncertainty has led to fragmented oversight & constrained innovation.

In other words, the bill is not simply trying to “allow blockchain”; it is trying to create a system where tokenised assets can exist within a formally regulated environment. This is an important distinction. Around the world, financial regulators are showing more comfort with tokenisation when it is tied to existing legal rights, regulated intermediaries, proper disclosures, identifiable issuers, compliant trading venues, & investor safeguards.

India’s proposed bill follows that same broad philosophy. Rather than treating tokenisation as something outside the financial system, it tries to bring it closer to the structures already familiar to regulators.

What the Bill Actually Covers

The proposal further identifies the key actors in such a market: issuers, custodians, token holders, trading platforms, regulatory authorities, & an inter-regulatory coordination committee. Together, these definitions show that the bill is not just a conceptual declaration.

It is structured as a market framework. It anticipates that tokenised assets will involve issuance, custody, listing, trading, execution, settlement, record keeping, disclosures, audits, disputes, enforcement, & appeals.

It also defines an asset token as a cryptographically secured digital representation of a right, title, interest, claim, or economic benefit in an underlying asset, generated, issued, stored, transferred, or traded using electronic means & recorded on distributed ledger technology or similar technology.

Perhaps the most important part of the bill is its attempt to provide legal recognition to asset tokens. The proposal states that asset tokens issued in accordance with the Act would be recognised as valid digital representations of rights, title, interest, claim, or economic benefit in the underlying asset.

That is a major step conceptually because tokenisation markets need more than technology to function at scale. They need legal enforceability. A token can only have real value if courts, regulators, investors, issuers, custodians, & market infrastructure participants know what legal right it carries & against whom that right can be enforced.

At the same time, the bill is careful not to oversimplify the relationship between a token & the underlying asset. It explicitly states that the issuance of an asset token does not automatically transfer ownership of the underlying asset unless such transfer is expressly provided in the tokenisation arrangement or in regulations under the Act.

The bill also says that rights, obligations, & entitlements attached to an asset token would be legally enforceable against the issuer & other relevant persons in accordance with disclosures, contractual terms, & regulatory requirements.

Who Would Regulate Tokenised Assets?

The bill specifically states that where issuance or trading of asset tokens involves securities, SEBI would be the principal regulatory authority. Where asset tokens involve payment systems, stable value arrangements, or banking-related activities, the RBI would exercise regulatory oversight. For insurance, pension, or other sectors, the respective statutory regulator would have jurisdiction.

This approach is important because tokenisation cuts across categories. A tokenised bond is not the same as tokenised real estate. A tokenised receivable platform is not the same as a stable-value settlement system. By proposing inter-regulatory coordination instead of a one-size-fits-all regulator, the bill acknowledges the hybrid nature of tokenised finance.

The bill places significant emphasis on conditions for issuance. No issuer may issue asset tokens unless it has legal ownership, control, or enforceable rights over the underlying asset; the asset is appropriately valued & verified; full, true, & fair disclosures are made; & the issuance complies with KYC, anti-money laundering, & anti-illicit activity safeguards.

The bill also requires an offering document before issuance. That aligns tokenised asset issuance with more traditional capital markets logic, where disclosures are essential to investor decision-making.

On the trading side, asset tokens would be traded only on registered platforms. Custody, meanwhile, would sit with registered custodians, & the bill requires segregation of client assets, proper records, & technological safeguards. Settlement & record keeping must also ensure transparency, auditability, & integrity of records.

I introduced a Private Member Bill titled The Asset Tokenisation (Regulation) Bill, 2026 in Parliament.

— Raghav Chadha (@raghav_chadha) March 14, 2026

The Bill is a forward-looking framework to bring legal clarity, transparency and investor protection to the emerging ecosystem of tokenised real-world assets in India.

Key… pic.twitter.com/P4NDEAYjtJ

For any tokenised asset framework to be taken seriously, investor protection has to be real. The bill appears to understand that. It provides for grievance redressal, transparency measures, fraud prevention, cyber security obligations, operational resilience, business continuity, audits, inspections, inquiries, civil penalties, criminal penalties, adjudication, & appeals.

Appeals would go to the Securities Appellate Tribunal, & the bill also includes adjudication procedures, transitional provisions for existing projects, & recognition of pilots or sandbox arrangements that may already have been permitted by regulators before the Act comes into force.

Why This Could Be Important for India’s Digital Finance Future

If India eventually develops a serious framework for tokenised real-world assets, the implications could be substantial. Tokenisation has the potential to improve asset accessibility, programmability, traceability, settlement efficiency, fractional ownership, & new market formats for capital formation. It could also create new infrastructure opportunities for fintech, market operators, custodians, compliance providers, & regulated digital asset rails.

As a Private Member Bill, the proposal does not automatically become law. It reflects a growing recognition that tokenisation is becoming too important to ignore. Whether India adopts this framework, modifies it heavily, or takes an entirely different route later, the discussion is now more concrete.

For now, the Asset Tokenisation (Regulation) Bill, 2026 stands as one of the clearest legislative attempts in India to define how tokenised real-world assets might be legally recognised, regulated, supervised, & enforced. And in a market increasingly shaped by the convergence of finance, law, & blockchain infrastructure, that conversation was always going to arrive sooner or later.

If you find any issues in this blog or notice any missing information, please feel free to reach out at yash@etherworld.co for clarifications or updates.

To promote your Web3 articles, events, and projects, you may reach out anytime via EtherWorld PR for submissions and collaboration.

Related Articles

- Indian Govt Launches Crypto Task Force Against Darknet Drug Trade

- Indian MP Raghav Chadha Pushes Crypto & Blockchain Reforms

- No Tax Relief for Crypto in India's Budget 2026

- Jio x Aptos: How India’s Giant Is Turning Web3 Into Everyday Utilityt

- Indian MP Flags Crypto Talent Drain Amid Heavy Taxation

To follow blockchain news, track Ethereum protocol progress, and read our latest stories, subscribe to our weekly today.

Disclaimer: The information contained in this website is for general informational purposes only. The content provided on this website, including articles, blog posts, opinions, & analysis related to blockchain technology & cryptocurrencies, is not intended as financial or investment advice. The website & its content should not be relied upon for making financial decisions. Read full disclaimer & privacy policy.

To stay updated on blockchain news, Ethereum protocol progress, and our latest stories, subscribe to our weekly digest and YouTube channel for ELI5 content.

To promote your Web3 articles, events, project updates, and Press Releases, reach out anytime via EtherWorld PR for submissions and collaboration. For other queries, email contact@etherworld.co.

If you’d like to support our work, share the content and consider donating at avarch.eth.

Join our community on Discord and follow us on Twitter, Facebook, LinkedIn & Instagram.

Author

Blockchain Content & Ops Specialist, Avarch LLC.