The Real Problem With Non-USD Stablecoins

Non-USD stablecoins continue to struggle on-chain because of FX volatility, unpredictable losses for LPs, and fragile liquidity.

Crypto has long promised a global financial system. Yet in practice, almost the entire on-chain economy runs on one currency: the United States dollar. Other fiat-linked stablecoins exist, including those pegged to the euro, Singapore dollar, Brazilian real, Japanese yen, and British pound.

But their on-chain presence is so small that it barely appears in system-wide charts. This week, two discussions explained why. One came from 0xAishwary, who has spent the entire year deploying foreign-exchange stablecoin pools. The other came from Artemis firm, whose stablecoin-supply chart went viral for showing the overwhelming dominance of USD-denominated assets.

These perspectives show that non-USD stablecoins are not failing because demand is absent. They are failing because existing liquidity infrastructure punishes anyone who tries to support them.

- The Pool That Broke Overnight

- Understanding Impermanent Loss

- What The Data Shows

- Why Polygon Became The Hub

- The New IL-Recovery Idea

- Why Solving This Matters

The Pool That Broke Overnight

Aishwary recently deployed a pool between XSGD and USDC. XSGD is a regulated Singapore-dollar stablecoin. The pool was created with a narrow concentrated-liquidity range that matched the real SGD to USD trading band. Nothing appeared risky.

The pool broke almost immediately. A routine shift in the SGD to USD exchange rate pushed the pair outside the selected range. This is normal in global FX markets.

On-chain, however, this small movement triggered a cascade. Arbitrage bots entered instantly, drained the XSGD side of the pool, and left only USDC behind.

By morning, the LP was left with real monetary loss. Fees earned were nowhere close to compensating for the harm. The entire XSGD allocation had vanished. This outcome is common for almost all non-USD pools deployed on AMMs.

One of the biggest challenge for non-USD stablecoins is not that that their demand doesn’t exist, it’s that they are volatile in nature.

— Aishwary (@0xAishwary) November 28, 2025

As someone who has been constantly working on fx on chain this entire year, and keeps deploying multiple currencies on chain daily, it is a… https://t.co/IRdCkbNynu

Understanding Impermanent Loss

The core challenge is impermanent loss. Impermanent loss is the difference between holding two assets outside a pool and holding them inside a pool after their price relationship changes.

AMMs rebalance positions automatically. If one currency appreciates and the other does not, the pool sells the stronger currency and buys the weaker one.

LPs end up with more of the asset that performed poorly and less of the asset that appreciated. In USD-to-USD pools, such as USDC against USDC.e, there is effectively no price divergence. IL becomes negligible.

In FX pairs, the currencies float independently. Even tiny movements create real IL. Bots capture every mispricing. The LP absorbs the loss. This creates an environment where returns cannot be predicted and participation becomes unsafe.

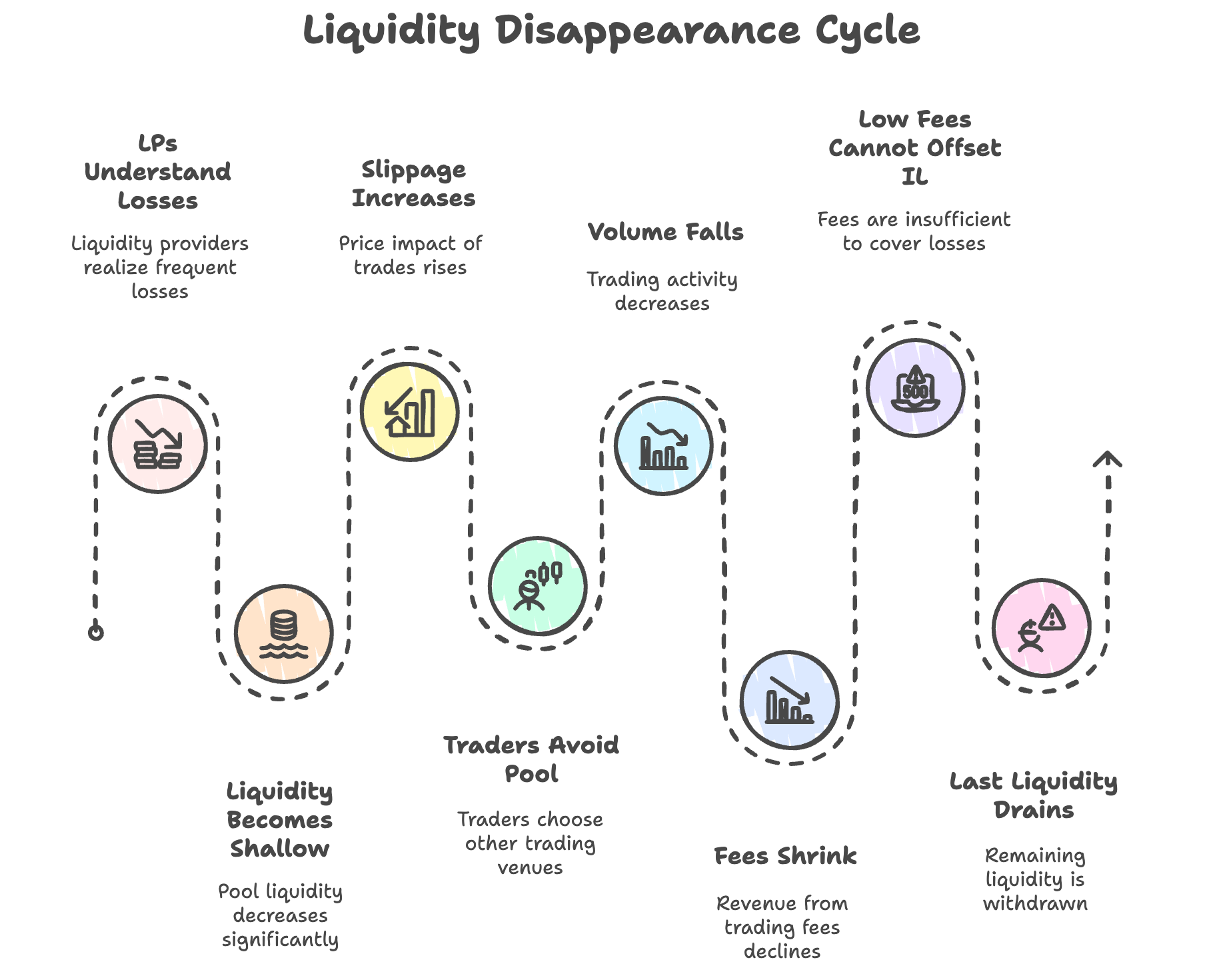

This is the central reason non-USD stablecoins struggle. Once LPs understand that losses are frequent and unpredictable, they exit the pools. When they exit, liquidity becomes shallow. When liquidity becomes shallow, slippage increases. When slippage increases, traders avoid the pool.

When traders avoid the pool, volume falls and fees shrink. Low fees cannot offset IL, and the last liquidity drains. This self-reinforcing cycle has prevented non-USD stablecoins from ever reaching meaningful adoption in DeFi.

What The Data Shows

Artemis published a striking chart. According to their October dataset, USD-denominated stablecoins account for almost all circulating supply. The euro sits far behind. Asian and Latin American currencies appear only as faint traces.

Many interpret this as evidence that nobody wants non-USD stablecoins. That conclusion ignores reality. Demand for foreign-currency rails exists everywhere outside crypto.

International sellers, exporters, gig workers, overseas students, regional ecommerce merchants, payroll systems, and remittance corridors all rely heavily on local currencies. The problem is not lack of need. The problem is that on-chain markets cannot hold these currencies without penalising liquidity providers.

Why Polygon Became The Hub

Aishwary points out that Polygon processes a large share of global non-USD stablecoin activity. This is not surprising. Polygon has low transaction fees, strong user bases in Asia and Latin America, and an ecosystem that encourages experimentation. It also integrates well with consumer-facing fintech applications that use local currencies.

Even so, non-USD pools on Polygon eventually collapse for the same reason. FX volatility interacts poorly with AMM design, and the incentives for LPs are not strong enough to withstand it. A supportive chain cannot fix a structural liquidity problem.

nobody wants non-USD stablecoins

— Artemis (@artemis) November 26, 2025

Five years, dozens of new issuers, every major currency tried, and none have made any progress in dethroning the dollar. https://t.co/rKzm3ltRXI pic.twitter.com/jrXwwlkL07

The New IL-Recovery Idea

This is where the discussion becomes interesting. After working through the problem with a liquidity strategist, Aishwary shared that a potential mechanism may allow liquidity providers in FX pools to recover their IL through the system itself.

The idea is not to eliminate IL. That is impossible when two currencies move independently. The idea is to make IL recoverable over time, allowing LPs to estimate returns even when FX prices shift. This would convert unpredictable losses into manageable risk.

If such a mechanism works, it could support:

- Stable yield for LPs

- Deeper liquidity for non-USD pairs

- Predictable risk for market makers

- Regional-fintech adoption

- Merchant payments in local currency

- Multi-currency remittance flows

- On-chain FX settlement

This would be the first structural solution that directly addresses the incentive problem at the heart of non-USD liquidity.

Why Solving This Matters

On-chain markets inherited the real world’s USD dominance. Global commodities, trade finance, and settlement rails rely heavily on the dollar. Crypto mirrored that structure without questioning whether it was optimal.

A functioning multi-currency layer would make on-chain finance more inclusive and more realistic. It would allow users in Asia, Africa, South America, and Europe to transact in their native currencies. It would also allow businesses to use stablecoin rails for cross-border operations without routing everything through USD.

For this to happen, liquidity providers must be able to participate in FX-based pools without unpredictable losses. Until that barrier is removed, non-USD stablecoins will continue to fail regardless of how many issuers enter the market.

The challenge facing non-USD stablecoins has never been about lack of demand. It has always been about misaligned incentives. The current AMM model exposes LPs to unavoidable FX volatility and frequent loss. Bots extract the remaining value. Liquidity evaporates. Adoption never begins.

The conversation initiated by Aishwary and supported by Artemis’ data shows that builders understand the real obstacle. More importantly, it suggests that a new framework for IL recovery might be possible. If liquidity providers can finally participate safely in non-USD pools, the on-chain economy may evolve from a dollar-only marketplace to a truly global one.

If you find any issues in this blog or notice any missing information, please feel free to reach out at yash@etherworld.co for clarifications or updates.

Related Articles

Disclaimer: The information contained in this website is for general informational purposes only. The content provided on this website, including articles, blog posts, opinions, & analysis related to blockchain technology & cryptocurrencies, is not intended as financial or investment advice. The website & its content should not be relied upon for making financial decisions. Read full disclaimer & privacy policy.

For Press Releases, project updates & guest posts publishing with us, email contact@etherworld.co.

Subscribe to EtherWorld YouTube channel for ELI5 content.

Share if you like the content. Donate at avarch.eth.

You've something to share with the blockchain community, join us on Discord!

Author

Blockchain Content & Ops Specialist, Avarch LLC.